Publications & Accepted Papers

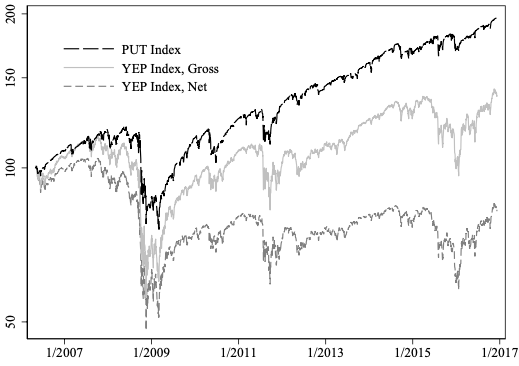

Engineering Lemons

Journal of Financial Economics, Volume 142, Issue 2, November 2021, Pages 737-755.

Paper, Online Appendix, SSRN Preprint, Video, Coverage by Alpha Architect

Abstract: Recent complex financial products sold to households contradict the basic premise of canonical innovation theories: financial innovation benefits its adopters. In my 2006–2015 sample of over 28,000 yield enhancement products (YEP) the securities offer attractive yields but negative returns. The products lose money both ex ante and ex post due to their embedded fees: on average, YEPs charge 6–7% in annual fees and subsequently lose 6–7% relative to risk-adjusted benchmarks. Simple and cheap combinations of listed options often statewise dominate YEPs. Competition, disclosure, or learning do not eliminate this inferior financial innovation over my sample period.

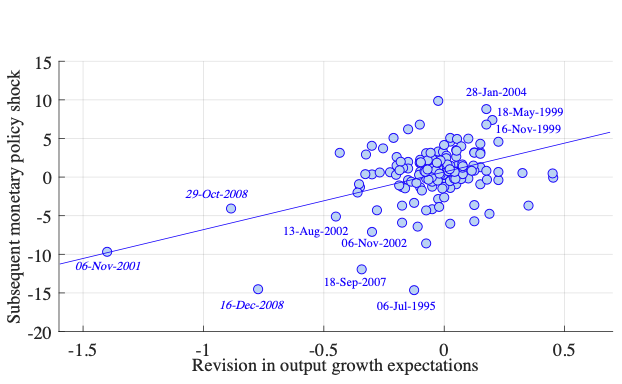

Growth Forecasts and News About Monetary Policy

with Nina Karnaukh, Journal of Financial Economics, Volume 146, Issue 1, October 2022, Pages 55-70.

Paper, SSRN Preprint, Orthogonalized MP shocks

Abstract: We find that 30-minute changes in bond yields around scheduled Federal Open Market Committee (FOMC) announcements are predictable with the pre-FOMC Blue Chip professionals’ revisions in GDP growth forecasts. A positive pre-FOMC GDP growth revision predicts a contractionary policy news shock (positive change in bond yields), a negative GDP growth revision predicts an expansionary policy news shock (negative change in bond yields). Failing to account for this predictability biases the estimates of monetary policy effects on the economy. First, the Fed’s information effect dissipates as the truly unpredictable policy news shock does not affect professionals’ beliefs about the economy. Second, net policy shock has a more negative impact on actual future GDP than the raw policy shock.

Labor income response relative to year before joining

Household Responses to Phantom Riches

with Samuli Knüpfer, Ville Rantala, and Erkki Vihriälä, Conditionally Accepted at Review of Financial Studies

November 2024 | SSRN Working Paper

Abstract: We study the consequences of investment fraud victimization using unique administrative data on Ponzi scheme investors. A matched control event-study design shows that the victims experience a 6% annual labor income loss. Income first declines when an investor joins the scheme, consistent with distorted beliefs lowering labor supply. The scheme’s collapse triggers a further decrease, which we attribute to financial stress caused by the collapse. Investors also face higher indebtedness and tilt their portfolios away from delegated investments. The income loss persists in the long run, equals twice the direct investment loss, and substantially adds to the social cost of fraud.

Working Papers

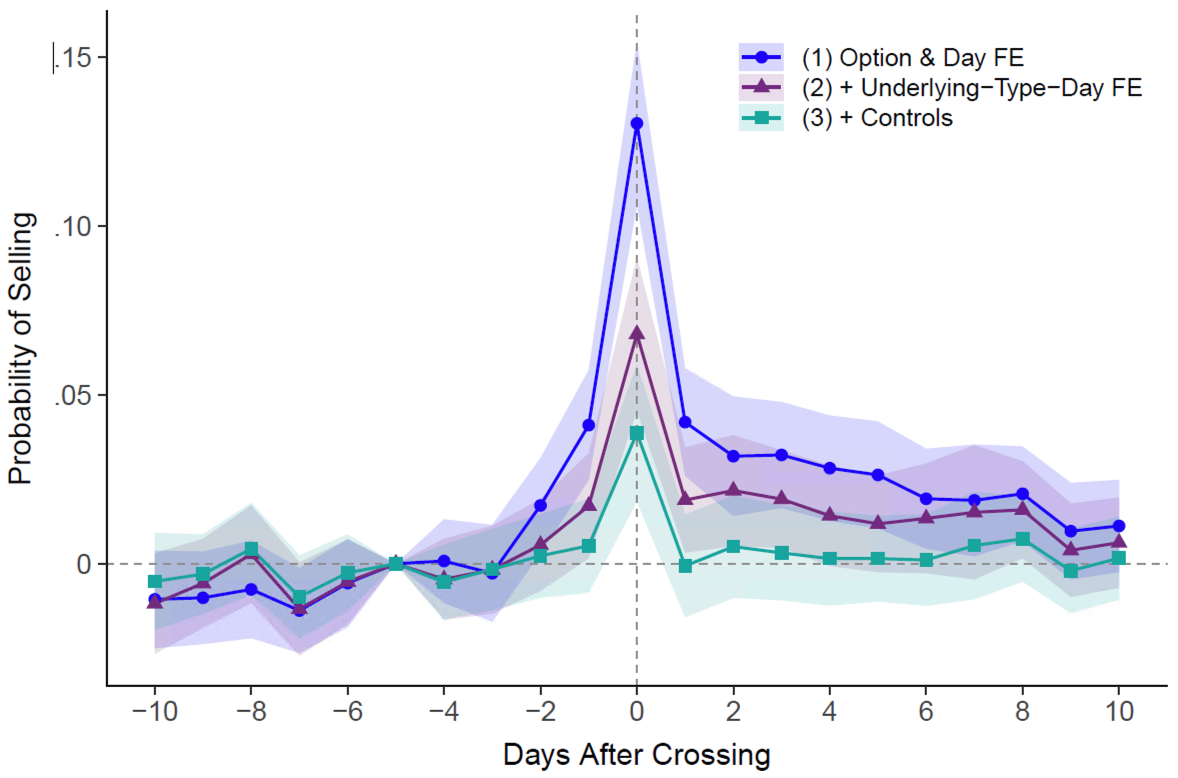

Propensity to Sell Options Around Strike Price Crossing

Investment TARGETS AS REFERENCE POINTS

with Aleksi Pitkäjärvi and Matteo Vacca

July 2026 | SSRN Working Paper

Abstract: We provide the first evidence of forward-looking reference points in investor behavior. Combining administrative data on option traders with a stacked difference-in-differences design, we show that investors' propensity to sell options spikes precisely when the underlying asset crosses the strike price, which retail investors frequently select to match their target price. The effect is difficult to explain using the standard disposition effect, nominal returns, salience, option Greeks, or complex option trading strategies. Moreover, the effect is present only for options bought out of the money, for which the strike price acts as a natural target, but absent for options bought in the money, for which it does not. The evidence is most consistent with investors evaluating gains and losses relative to a forward-looking target, in sharp contrast with the backward-looking purchase price widely used in the disposition effect literature. Our findings suggest that standard tests of reference dependence in selling decisions are misspecified when investors evaluate outcomes relative to reference points other than the purchase price.

Conferences: Tilburg Finance Summit, Helsinki Finance Summit, Northern Finance Association, Derivatives and Asset Pricing Conference, SRP and Derivatives Conference, EFA, MFA, SGF, International Behavioural Finance Conference (London), NFN, RBFC

Democratizing Private Markets: Private Equity Performance of Individual Investors

with Cynthia Balloch, Federico Mainardi, and Simon Oh

June 2025 | SSRN Working Paper, Slides | Coverage by SEC Commissioner Uyeda

Abstract: Using new data on wealthy U.S. households, we provide the first systematic study of private equity performance by individual investors. We identify two innovations that democratize access to private equity: the proliferation of funds with low minimum commitments and pooling capital via advisors. Contrary to concerns about poor performance, we find that aggregate individual investments in private equity perform similarly to institutions and outperform public markets. In the cross-section, the most affluent investors outperform the less affluent by 6 to 10 percentage points in public market equivalent. We show that advisor skill is more likely to explain the performance gap rather than preferential access. Using both observed and simulated intermediary fees, we show that fees impose a sizable drag on performance, especially for less affluent investors.

Conferences: American Finance Association 2027; Western Finance Association; European Finance Association; RCFS Winter Conference; Columbia PE Conference; Aalto Institutional Investor Conference (Helsinki); IPC Alternative Investments Conference & Spring Research Symposium 2025; 12th Annual Conference on Financial Market Regulation (SEC); Private Capital Symposium (LBS); UT Dallas Finance Conference; Finance, Organizations and Markets Conference (USC); 2025 Private Firm Symposium (U Chicago); UBC Winter Finance Conference; Loyola Wealth Management Conference; Mid-Atlantic Research Conference; LUISS Finance Workshop; SHoF Annual Conference on the Future of Private Capital Markets

Juicing the Coupon Yield: How Banks Extract Rents from Behavioral Biases

July 2025 | SSRN Working Paper

Abstract: The fees on yield enhancement products increase strongly with coupons, despite minimal pass-through of coupons to returns. As a result, higher coupons paradoxically lead to lower net expected returns. Demand estimates exploiting pricing shocks show investors pay over 35 basis points for one percentage point of coupon. Banks engineer coupons using exotic, hard-to-value options that artificially increase coupons, but much less so returns. These patterns are inconsistent with standard reaching-for-yield models and instead point to investor inattention to shrouded attributes. I show that the resulting rents extracted by banks are several times larger than those documented in other financial markets.

NFA 2023 Best Paper Award in Asset Pricing and Market Microstructure

Conferences: AFA (San Antonio), NBER Behavioral Finance, CEPR Workshop on Household Finance, Finance Down Under, Virtual Derivatives Workshop, HEC-McGill Winter Finance Workshop, SGF, MFA, WAPFIN @ NYU, CFPB Research Conference, NFA, CDI

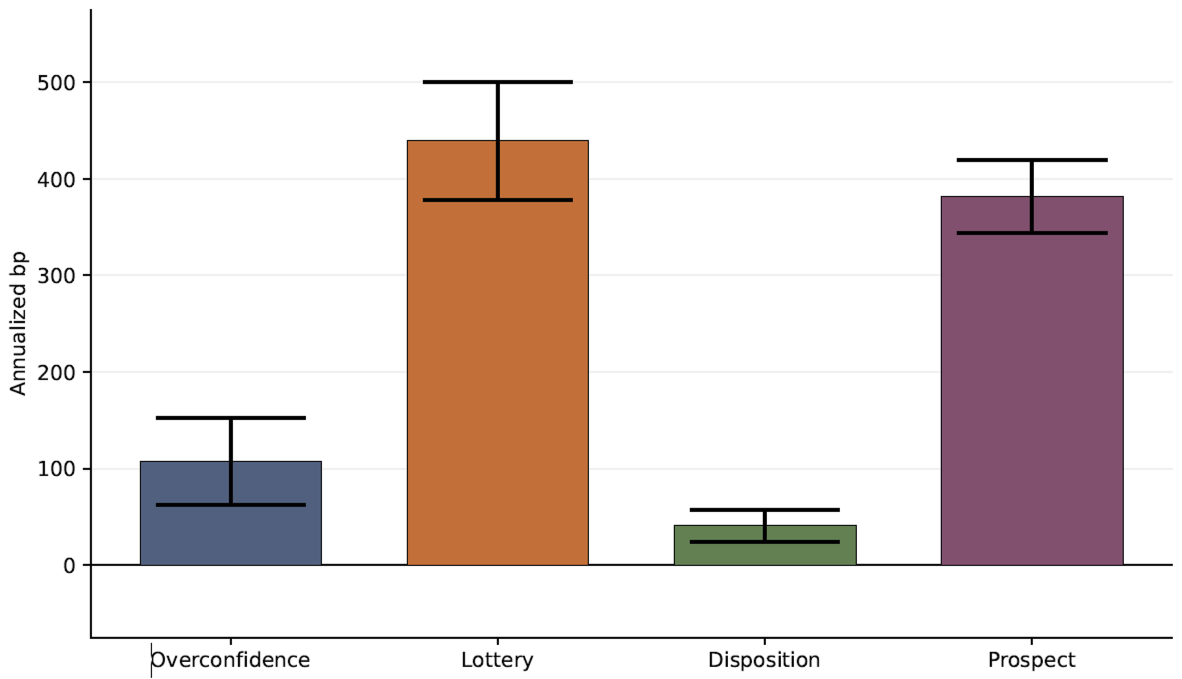

Average Anomaly Contribution

DO HOUSEHOLD BIASES MATTER FOR ASSET PRICES?

with Carter Davis, Samuli Knüpfer, Jens Soerlie Kvaerner, Bahar Sen-Dogan

July 2026 | SSRN Working Paper

Abstract: Are household behavioral biases quantitatively important for asset prices? We answer this question using complete ownership records for Norwegian stocks from 2007 to 2020 and a demand-system model of asset prices. Households account for 1.8 times their market share of cross-sectional return variation. Wealthy investors with strong behavioral tilts drive most of this effect. These households are also anomaly creators: within each bias family, reallocating capital from the most-biased households to the least-biased households compresses anomaly spreads, with the strongest effects among households with prospect-theory and lottery tilts. Our results provide quantitative evidence for a central premise of behavioral asset-pricing models: behavioral biases matter in the aggregate and affect the equilibrium pricing of stock-market anomalies.

Conferences: CEPR European Conference on Household Finance (Stockholm), European Finance Association, Midwest Finance Association, Northern Finance Association, Nordic Household Finance Summit